[ad_1]

In these instances, double down — in your abilities, in your information, on you. Be a part of us Aug. 8-10 at Inman Join Las Vegas to lean into the shift and be taught from the most effective. Get your ticket now for the most effective value.

Mortgage servicing big Mr. Cooper continues to make inroads on its quest to construct a $1 trillion mortgage servicing portfolio — which it intends to wring most income from by changing many name heart staff with synthetic intelligence and by getting a soar begin on different lenders when householders are able to refinance.

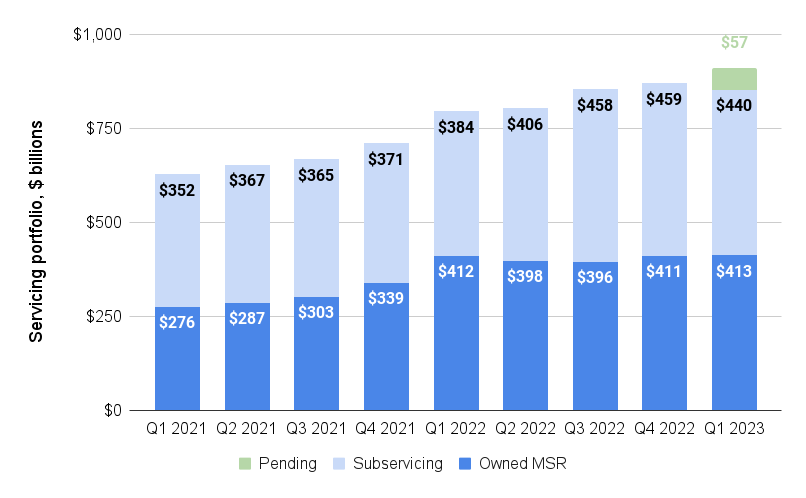

In reporting a $37 million first-quarter internet revenue Wednesday, Dallas, Texas-based Mr. Cooper stated it grew its mortgage servicing portfolio — mortgages it collects funds on, on behalf of traders — by 7 p.c from a yr in the past to $853 billion.

That determine doesn’t embrace a further $57 billion in mortgage servicing rights for which Mr. Cooper has not too long ago signed offers. Add these pending offers to the combo, and Mr. Cooper will quickly be servicing greater than $900 billion in mortgage debt.

Mr. Cooper’s servicing portfolio approaching $1T

Mr. Cooper mortgage servicing rights (MSR) portfolio in billions of {dollars} | Supply: Mr. Cooper regulatory filings

That’s regardless of dropping $30 billion in subservicing rights throughout the first quarter to a shopper that acquired their very own servicing platform and is taking their mortgage portfolio in-house, Mr. Cooper Vice Chairman and President Christopher Marshall stated on a name with funding analysts.

Mr. Cooper’s subservicing portfolio — loans that the corporate collects funds on beneath contract with lenders who retain possession of these servicing rights — shrank by 4 p.c from the fourth quarter to $440 billion.

Chris Marshall

“You might see extra volatility in our complete e-book over the steadiness of the yr,” Marshall stated. “However total, we really feel nice about our subservicing enterprise, and I’d observe that we’ve already changed a considerable portion of this loss with development from different shoppers.”

Pending acquisitions of Rushmore Mortgage Administration Companies LLC’s $37 billion mortgage subservicing platform, together with an earlier settlement to amass mum or dad firm Roosevelt Administration Firm LLC, are anticipated to shut by midyear. Marshall stated Mr. Cooper will onboard “a number of hundred individuals” as a part of the deal.

Mr. Cooper’s owned mortgage servicing rights (owned MSR) portfolio grew by simply $2 billion from the earlier quarter to $413 billion — about the place it was a yr in the past.

Though Mr. Cooper Chairman and CEO Jay Bray stated the corporate expects to make “a whole lot of progress” this yr towards the corporate’s aim of constructing a $1 trillion servicing portfolio, he additionally pegged that quantity as “an absolute minimal for the place we will go” in the long term.

Jay Bray

“The alternatives we’re seeing proper now are as thrilling as something we’ve checked out in latest reminiscence, and I count on us to exit this a part of the cycle as a bigger, extra worthwhile and much more dominant competitor,” Bray stated on a name with funding analysts.

Mortgage servicers can earn cash in two methods — by gathering charges from the traders who truly personal the mortgages they gather fee on and by offering loans when householders are able to refinance.

When rates of interest rise, mortgage servicers make much less cash refinancing, however the worth of their mortgage servicing rights will increase, as a result of debtors are much less more likely to refinance out of their servicing portfolio.

Bray stated Mr. Cooper — which slashed greater than 1,000 jobs final yr as originations dwindled — thinks it could possibly trim at the very least $50 million in annual bills from its name facilities through the use of synthetic intelligence to deal with buyer calls.

Mr. Cooper has made a “huge funding” in interactive voice response (IVR) to take buyer calls utilizing AI, Bray stated.

“If you consider what we’re attempting to do, it’s actually to copy the Amazon mannequin,” Bray stated. “I’m positive everybody on this name makes use of Amazon and but I doubt anybody has ever spoken to anybody at Amazon. That’s since you don’t need to.”

Bray stated Mr. Cooper spends “a number of hundred million {dollars} a yr” on name heart operations and expects to realize $50 million in annual financial savings on the outset of what’s anticipated to be “a multiyear challenge.”

“We have now a whole lot of work forward of us, however we predict it’s a giant alternative, huge alternative not simply to remove expense however to make the expertise a lot, significantly better for our clients,” Bray stated.

Mortgage originations dwindle

Mr. Cooper mortgage originations by channel, in billions of {dollars} | Supply: Mr. Cooper regulatory filings

One other means Mr. Cooper expects to revenue from its rising mortgage rights servicing portfolio is by offering loans when householders are able to refinance or purchase their subsequent house — incomes charges because the mortgage originator and holding the borrower within the firm’s servicing portfolio.

Mr. Cooper acquires mortgages originated by correspondent lenders, and likewise “recaptures” debtors by providing refinancing on to householders from which it’s gathering funds. Marshall stated Mr. Cooper’s recapture fee is about double the {industry} fee.

“For somebody who has already completed a transaction with us that we’ve already refinanced, we seize approaching 80 p.c,” he stated.

Whereas Mr. Cooper’s mortgage originations enterprise has largely dried up — the $2.7 billion in first quarter originations represented an 89 p.c drop from two years in the past — the corporate expects lending to select up when the financial system cools and rates of interest come again down.

“You’ve seen us display industry-leading recapture charges quarter over quarter, yr after yr, and you already know that on the proper level within the cycle, we will generate origination income properly over $1 billion,” Bray stated. “A key a part of our technique is to maintain investing in our direct-to-consumer platform in order that we’re able at any time when the cycle turns, to do much more.”

Xome REO stock and gross sales climb

Xome stock and gross sales, by quarter | Supply: Mr. Cooper regulatory filings

Along with servicing and originating mortgages, Mr. Cooper’s Xome subsidiary operates an public sale platform for foreclosed and real-estate-owned (REO) properties.

Throughout the first quarter of 2023, stock on the platform climbed 48 p.c from a yr in the past to 27,003 houses. Gross sales have been up 26 p.c from a yr in the past to 1,494, surpassing the 2022 peak of 1,285.

Marshall stated Xome is on observe to change into worthwhile within the second half of the yr as properties flowed onto the platform at a document tempo in March.

“A part of that is companies getting extra snug with their compliance processes, however our group has additionally been actively promoting to new clients,” Marshall stated. “And consequently, our market share of Ginnie Mae foreclosures is now rising above the 40 p.c goal we laid out for you a yr in the past.”

Whereas Marshall has stated previously that Mr. Cooper has been in discussions with potential traders about spinning off Xome, he didn’t present additional insights on Wednesday’s name.

Noting that the 37 p.c quarterly development in Xome gross sales was according to our projections, he stated Mr. Cooper expects that quantity to develop once more within the second quarter.

“We’re seeing extra investor exercise on the alternate, which incorporates extra visits to our web site, stronger bidding exercise, extra bids per asset and enhancing pull-through charges,” Marshall stated.

Get Inman’s Mortgage Transient Publication delivered proper to your inbox. A weekly roundup of all the largest information on the earth of mortgages and closings delivered each Wednesday. Click on right here to subscribe.

E-mail Matt Carter

[ad_2]

Source link