[ad_1]

It’s no marvel why cell publishers are battling to maintain extra of their subscription income out of the arms of platforms like Apple and Google — a brand new report signifies the highest 100 non-game, subscription-based apps noticed their shopper spend improve 41% in 2021 to $18.3 billion, up from $13 billion in 2020.

And this represents only a small portion (14%) of the general income from in-app purchases throughout each apps and video games, which totaled $131.6 billion in 2021, based on this newest knowledge from app intelligence agency Sensor Tower.

Nevertheless, this group’s portion of the market is rising. In 2020, subscription income in non-game apps represented simply 11.7% of the whole shopper spend for the yr, for comparability.

Picture Credit: Sensor Tower

The report additionally famous the 41% year-over-year improve in in-app buy income in 2021 represented stronger development than the 34% development charge between 2019 and 2020.

In fact, the worldwide coronavirus pandemic might have performed a job right here. In 2020 and past, shoppers more and more turned to apps for procuring, leisure, well being and health, work, training, and extra because the world tailored to lockdown measures, digital work and education, and started to do extra of their previously in-person actions on-line — like procuring or occasions, for instance.

The U.S. figures mirrored the worldwide traits when it got here to cell spending on subscriptions, the information confirmed. Final yr, U.S. shoppers spent $8.5 billion within the high 100 non-game subscription apps, up 44% from $5.9 billion in 2020 — extra sizable development than the 28% rise seen the yr prior. In whole, U.S. shoppers spent $40.7 billion on in-app purchases in 2021.

Picture Credit: Sensor Tower

Subscriptions have additionally change into the dominant technique of driving app retailer income. Within the fourth quarter, 90 out of the highest 100 top-grossing U.S. apps included a subscription. This determine is simply barely down from the 91 in This fall 2020 or the 93 in This fall 2019.

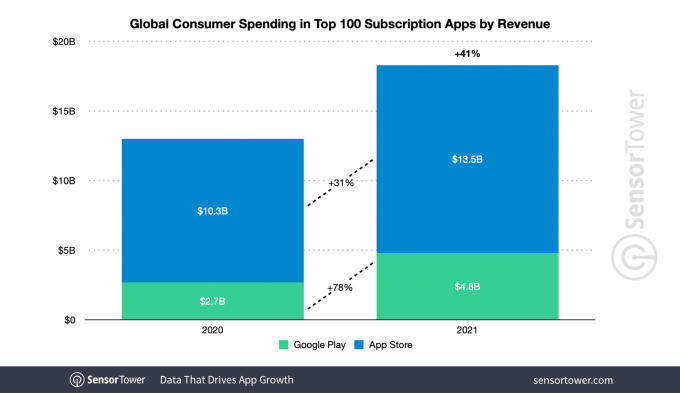

Apple’s App Retailer continues to outpace Google Play in the case of subscription income. Final yr, the highest 100 non-game subscription apps on the App Retailer noticed almost thrice as a lot spending as these on Google Play, at $13.5 billion versus $4.8 billion, respectively. This represented 31% year-over-year development from $10.3 billion for a similar group on the App Retailer in 2020, and 78% development from the $2.7 billion for the group on Google Play.

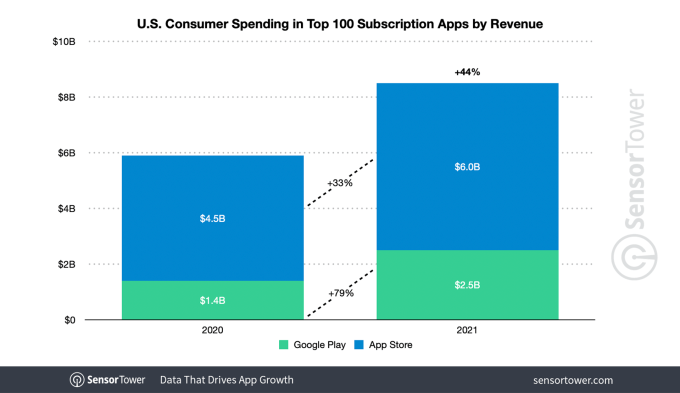

The U.S., once more, noticed an analogous development. Right here, the highest 100 subscription apps on the App Retailer grew 33% year-over-year from $4.5 billion in 2020 to succeed in $6 billion in 2021. Subscription apps on Google Play, in the meantime, grew 79% from $1.4 billion in 2020 to succeed in $2.5 billion in 2021.

Picture Credit: Sensor Tower

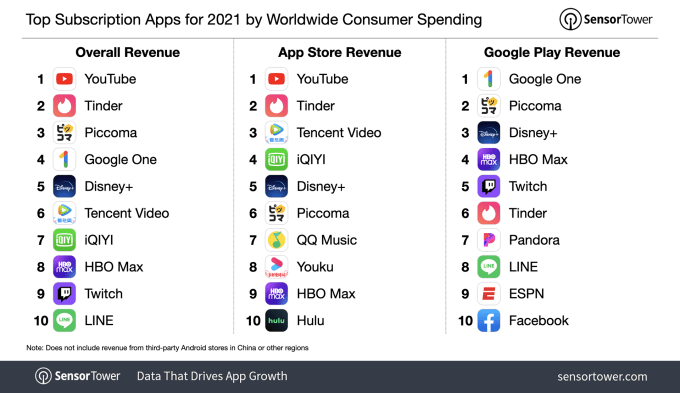

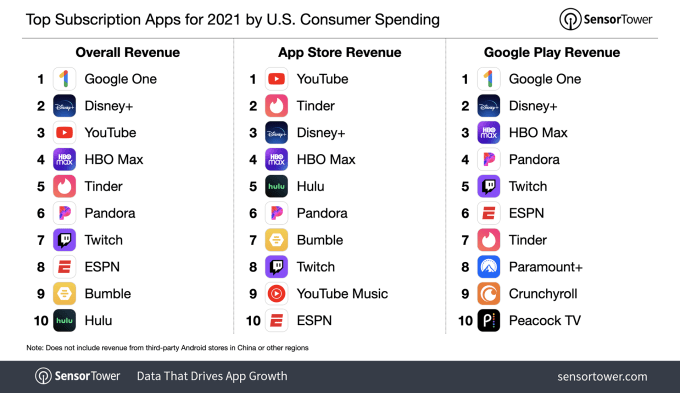

Google’s apps high the charts, alongside different streaming and relationship apps, in the case of shopper spending. Google’s subscription service Google One made $1.1 billion worldwide final yr through its app, $698 million of which was from the U.S.. And Google’s YouTube app made $1.2 billion final yr, $566.5 million of which was from the U.S.

Different top-grossing U.S. apps included Disney+, HBO Max, and Tinder. Worldwide, you may add Piccoma to that listing.

Picture Credit: Sensor Tower

Evaluation of the subscription market like that is attention-grabbing given the elevated regulatory scrutiny of the apps shops’ enterprise fashions over the previous yr.

Some markets, like South Korea, even handed new legal guidelines to restrict Apple and Google’s management over in-app purchases. Presently, Dutch regulators are in a standoff with Apple over relationship apps’ funds, claiming Apple is in violation of anti-trust orders. And whereas this knowledge is simply analyzing the non-gaming traits, the cash that app shops make from gaming corporations can be large — which is why Epic Video games, as an example, is interesting the courtroom’s determination in its personal antitrust case.

[ad_2]

Source link