[ad_1]

For American restaurant chains, the early months of the pandemic have been a difficult interval. However quickly issues modified for the higher as folks began ordering their favourite meals gadgets on-line throughout the lockdown, triggering a gross sales growth. Market leaders, together with McDonald’s, Starbucks, and Chipotle Mexican Grill, ramped up their supply, curbside pickup, and drive-thru companies to cater to the spike in orders.

The businesses’ resilience to headwinds like COVID-19 is a testomony to the recognition of their inexpensive, quick-service meals and modern menus. They give the impression of being poised to capitalize on their capacity to adapt to adjustments in working circumstances and clients’ cravings for tasty ready-to-eat meals. These elements allow the businesses to carry out higher than their ‘formal’ counterparts that rely on dine-in clients.

Buyer is King

Come 2023, the state of affairs is totally different – market reopening has introduced clients again to eating places and the virus-induced house supply growth waned. It will be attention-grabbing to investigate the place the business is headed this yr because it faces new challenges like tightening client spending amid excessive inflation and rising rates of interest.

The benefit of the multichannel shift is that restaurant operators can now leverage each their revamped supply amenities in addition to conventional dine-in companies to serve clients higher. The financial stoop is unlikely to impression their companies within the foreseeable future, because of aggressive pricing and the fast-food tradition ingrained within the minds of individuals.

The comfort led to by on-the-go snacks and prepared meals is irresistible to nearly all classes of individuals, who would proceed visiting quick meals eating places regardless of their monetary well-being. With market circumstances changing into increasingly conducive to the franchise enterprise mannequin, restaurant operators can now broaden to new markets with ease.

Burger Large

McDonald’s Company (NYSE: MCD), the most important snack chain within the US by way of market capitalization, has maintained secure gross sales and earnings progress nearly in each quarter because the onset of the pandemic, regardless of closing a number of eating places, primarily in Russia. Final yr, comparable gross sales bounced again from an preliminary stoop, with gross sales selecting up at each company-operated and franchised eating places.

After peaking a number of months in the past, MCD is at the moment buying and selling at a premium. The corporate is investing closely in revamping its retailer community and including new models, which might catalyze gross sales progress. This optimistic backdrop would enable the corporate to proceed returning worth to shareholders, which makes the inventory a superb guess.

The Excellent Brew

Espresso chain Starbucks Company (NASDAQ: SBUX) has consistently maintained its dominance within the extremely aggressive ready-to-drink market. The corporate had its share of issues quickly after the pandemic outbreak, however the administration took aggressive steps to align the enterprise with new tendencies – like pushing extra merchandise by means of retail shops and e-commerce platforms like Amazon, in order to succeed in even these clients who may not be visiting its outlet.

In an effort to capitalize on the success of its partnership with Nestle, which helped broaden the non-core Channel Improvement enterprise, the corporate is extending the tie-up to new merchandise and markets. It seems to beat inflation by elevating costs and defending margins however that’s unlikely to have an effect on gross sales volumes.

After getting into 2023 on a excessive notice, Starbucks’ inventory pared part of the positive aspects and is at the moment buying and selling under $100. The dip in valuation might be seen as a superb entry level, given the espresso big’s promising progress prospects. Going ahead, reopening in China, one of many firm’s key markets, would add to gross sales and margin progress. So, SBUX now has all the things it takes to create sturdy shareholder worth.

Mexican Delicacies

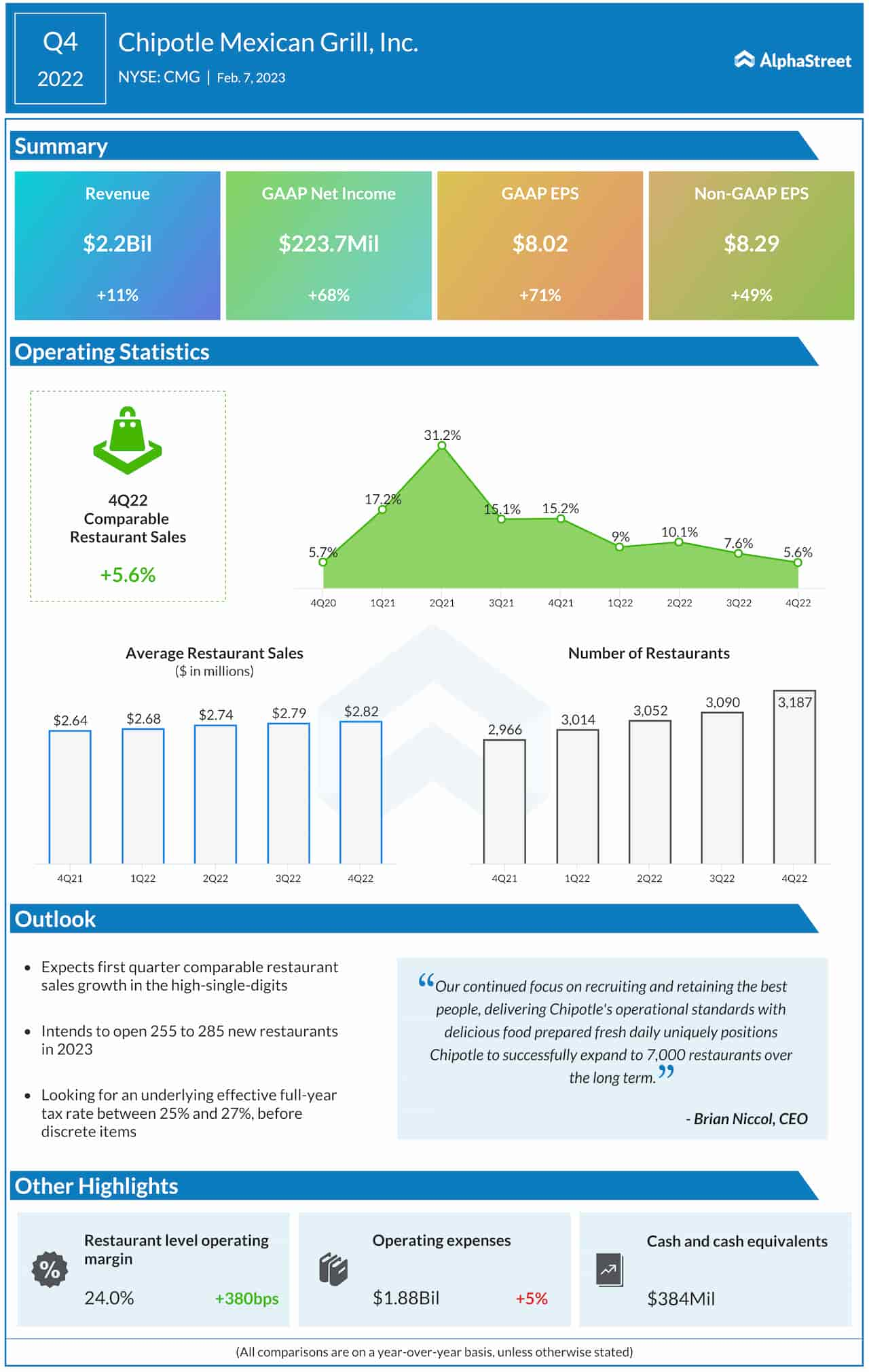

Chipotle Mexican Grill (NYSE: CMG) is a fast-casual restaurant chain specializing in made-to-order bowls, tacos, and burritos. Having efficiently navigated the pandemic, the corporate hiked costs and has been in a position to develop gross sales and revenue with out affecting demand, supported by its extremely loyal clients. Over the previous 5 years, it delivered stronger-than-expected earnings in nearly each quarter, whereas rising gross sales consistently.

Of late, Chipotle has been including new models to its restaurant community at a quick tempo. That has helped the corporate ship double-digit gross sales progress in latest quarters, a development that’s anticipated to proceed because the administration is planning to speak in confidence to 285 eating places this yr. Within the fourth quarter, adjusted earnings rose a whopping 50%. In the entire of FY22, working margin climbed to 13.4%, displaying that Chipotle is firing on all cylinders.

CMG is among the most costly fast-food shares, with a 52-week common worth of about $1,500. But, the present valuation is engaging from the long-term funding perspective as a result of the inventory is unlikely to develop into cheaper anytime quickly.

[ad_2]

Source link